Arts

DEMAND Intensifies For CONTEMPORARY ART As SUPPLY CONTRACTS And PRICES Rise

H1 2019 Art Market Report

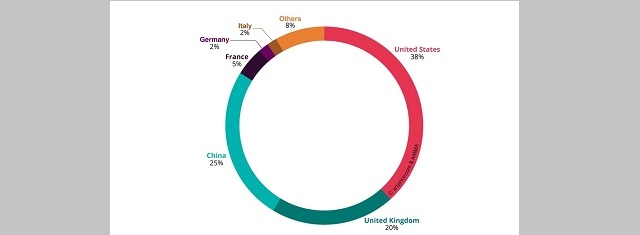

Geog. distribution of the Fine Art auction H1 2019 (Source: Artprice.com)

Geog. distribution of the Fine Art auction H1 2019

(Source: Artprice.com)

(Source: Artprice.com)

2 - Average annual ROI worked out at +4.6% for an average holding of 13 years

3 - Tighter supply pushed prices up

4 - The volume des Fine Art* transactions was up very slightly: +0.1%

5 - The USA (-20%), China** (-12%) and the UK (-25%) all posted lower turnover

6 - The Artprice100© index posted a 16% growth in H1 2019

7 - Top quality Modern (-21%) and Old Master (-38%) works in short supply

8 - Claude Monet dominated H1 2019 with 23 works sold generating €251 million

9 - New record for a living artist: Jeff Koons' Rabbit (1986) fetched $91 million

1- Prices of Contemporary Art were up 40%

2 - Average annual ROI worked out at +4.6% for an average holding of 13 years

3 - Tighter supply pushed prices up

4 - The volume des Fine Art* transactions was up very slightly: +0.1%

5 - The USA (-20%), China** (-12%) and the UK (-25%) all posted lower turnover

6 - The Artprice100© index posted a 16% growth in H1 2019

7 - Top quality Modern (-21%) and Old Master (-38%) works in short supply

8 - Claude Monet dominated H1 2019 with 23 works sold generating €251 million

9 - New record for a living artist: Jeff Koons' Rabbit (1986) fetched $91 million

2 - Average annual ROI worked out at +4.6% for an average holding of 13 years

3 - Tighter supply pushed prices up

4 - The volume des Fine Art* transactions was up very slightly: +0.1%

5 - The USA (-20%), China** (-12%) and the UK (-25%) all posted lower turnover

6 - The Artprice100© index posted a 16% growth in H1 2019

7 - Top quality Modern (-21%) and Old Master (-38%) works in short supply

8 - Claude Monet dominated H1 2019 with 23 works sold generating €251 million

9 - New record for a living artist: Jeff Koons' Rabbit (1986) fetched $91 million

- General conclusion“¦

* With the collaboration of its Chinese State partner AMMA (Art Market Monitor of Artron), Artprice identified 262,300 Fine Art lots sold via public sales around the world in the first half of 2019. Together, these transactions generated a total of $6.98 billion, down 17.4% versus H1 2018

* However, Artprice's price index calculation, based on our 'repeat sales method', shows a 5% increase in art prices. With the banking sector operating in a negative or near-zero interest rate environment, the ROI in art is bound to add momentum to the market's expansion.

* "We are seeing a tightening of the balance between supply and demand in the Art Market," explains thierry Ehrmann, Artprice's Founder/CEO

* "The results show persistent demand for museum-quality artworks, but the secondary market's supply has tightened somewhat. The Art Market ““ as it has developed since 1975 ““ appears to be reaching its structural limits: auction houses are struggling to maintain their operating margins and also to convince collectors to sell their best pieces.

* With the collaboration of its Chinese State partner AMMA (Art Market Monitor of Artron), Artprice identified 262,300 Fine Art lots sold via public sales around the world in the first half of 2019. Together, these transactions generated a total of $6.98 billion, down 17.4% versus H1 2018

* However, Artprice's price index calculation, based on our 'repeat sales method', shows a 5% increase in art prices. With the banking sector operating in a negative or near-zero interest rate environment, the ROI in art is bound to add momentum to the market's expansion.

* "We are seeing a tightening of the balance between supply and demand in the Art Market," explains thierry Ehrmann, Artprice's Founder/CEO

* "The results show persistent demand for museum-quality artworks, but the secondary market's supply has tightened somewhat. The Art Market ““ as it has developed since 1975 ““ appears to be reaching its structural limits: auction houses are struggling to maintain their operating margins and also to convince collectors to sell their best pieces.

* They are constantly increasing their buyer fees while simultaneously inventing new ways of reassuring sellers. Guarantees can encourage some sales, but this mechanism doesn't represent a global solution. It's time for the Art Market to start a new era".

* The recent acquisition of Sotheby's and Artprice.com's metamorphosis into Artmarket.com (new name and corresponding AoA amendments submitted to an EGM in September 2019) are two changes that clearly reflect the Art Market's entry into the digital age.

- Global figures

* At a global level, more than 262,300 Fine Art lots were auctioned in the first six months of 2019, up 0.1% on H1 2018.

* Artprice, world leader in Art Market information since 1987, has systematically analysed the results of more than 3,502 auction sales (3,532 in H1 2018) around the world. This half-year report covers public sales of Fine Art (painting, sculpture, drawing, photography, prints and installations).

* The recent acquisition of Sotheby's and Artprice.com's metamorphosis into Artmarket.com (new name and corresponding AoA amendments submitted to an EGM in September 2019) are two changes that clearly reflect the Art Market's entry into the digital age.

- Global figures

* At a global level, more than 262,300 Fine Art lots were auctioned in the first six months of 2019, up 0.1% on H1 2018.

* Artprice, world leader in Art Market information since 1987, has systematically analysed the results of more than 3,502 auction sales (3,532 in H1 2018) around the world. This half-year report covers public sales of Fine Art (painting, sculpture, drawing, photography, prints and installations).

* According to thierry Ehrmann, Artprice's founder/CEO, "Since 2000, the Art Market has shown an exceptionally high level of maturity resisting the NASDAQ crisis, the consequences of 9/11, the second Iraq war, and an unprecedented financial and economic crisis that has plunged the developed world into a long-term low interest rates environment undermining the value of savings. It is now resisting a global context of heightening geopolitical tensions between China and the USA. During these past 19 years, the Art Market has managed to adapt to reality, not only avoiding its own collapse, but actually creating a genuine investment safe-haven“¦ without forming a speculative bubble."

* The attractive returns on art over the last few years have outperformed many other investments, and the Art Market has become an independent, liquid and efficient market on all continents.

* As mentioned, our Artprice100© index is showing 16% growth for H1 2019.

* The attractive returns on art over the last few years have outperformed many other investments, and the Art Market has become an independent, liquid and efficient market on all continents.

* As mentioned, our Artprice100© index is showing 16% growth for H1 2019.

- Top 10 Countries by Auction Turnover ““ H1 2019

* Country --- Turnover --- (Market Share)

1 - United States - $2,677,834,700 (38.4%)

2 - China - $1,762,874,600 (25.3%)

3 - UK - $1,408,229,500 (20.2%)

4 - France - $329,649,500 (4.7%)

5 - Germany - $131,566,800 (1.9%)

6 - Italy - $108,472,900 (1.6%)

7 - Switzerland - $70,280,000 (1.0%)

8 - Japan - $52,772,400 (0.8%)

9 - Austria - $49,982,800 (0.7%)

10 - Australia - $32,264,300 (0.5%)

* The data for the Chinese art market is the fruit of Artprice's 11-year collaboration with its Chinese institutional partner, Artron Group and AMMA (Art Market Monitor by Artron), directed by Wan Jie.

* Despite economic disparities and uncertainties, the global art market has shown signs of buoyancy, driven by a powerful combination of investment logic, speculative buying, passion collecting and insatiable demand for major signatures from new museums around the world.

* Country --- Turnover --- (Market Share)

1 - United States - $2,677,834,700 (38.4%)

2 - China - $1,762,874,600 (25.3%)

3 - UK - $1,408,229,500 (20.2%)

4 - France - $329,649,500 (4.7%)

5 - Germany - $131,566,800 (1.9%)

6 - Italy - $108,472,900 (1.6%)

7 - Switzerland - $70,280,000 (1.0%)

8 - Japan - $52,772,400 (0.8%)

9 - Austria - $49,982,800 (0.7%)

10 - Australia - $32,264,300 (0.5%)

* The data for the Chinese art market is the fruit of Artprice's 11-year collaboration with its Chinese institutional partner, Artron Group and AMMA (Art Market Monitor by Artron), directed by Wan Jie.

* Despite economic disparities and uncertainties, the global art market has shown signs of buoyancy, driven by a powerful combination of investment logic, speculative buying, passion collecting and insatiable demand for major signatures from new museums around the world.

* These growth drivers rely heavily on easy access to reliable Art Market information such as that provided by Artprice ““ a pioneer and global leader in the field ““ and have been boosted by a whole series of underlying phenomena. These include a rapidly spreading awareness that every aspect of participation in the art market, including online sales, can be conducted via the Internet (97% of participants are connected to the Internet); the financialisation of the art market's high-end fostered by its stability and transparency; a rapid increase in the art-buying population from roughly 500,000 after 1945 to approximately 70 million in 2016; a significant reduction in the average age of market participants and a geographical expansion of the market to nearly all of Asia, the Pacific Rim, India, South Africa, the Middle-East and South America.

* Another important driver of the global Art Market is the new-era museum industry (700 new museums per year) that has become a significant economic reality in the 21st century. More museums have opened since 2000 than in the previous two centuries.

* Hungry for 'museum quality' works, this sector is one of the primary drivers of the Art Market's spectacular growth. The Art Market is now both mature and liquid, offering yields of 9% to 14% p.a. on works valued over $100,000.

* With central banks effectively working in a negative or near-zero interest rate environment, the Art Market looks very healthy by comparison, having posted a 1,955% growth in the annual auction turnover of its Contemporary segment over the past 19 years.

* These returns are not just reserved for 'star' artists. Our research finds a substantial average annual yield of approximately 7% on works sold above the €20,000 threshold.

* Hungry for 'museum quality' works, this sector is one of the primary drivers of the Art Market's spectacular growth. The Art Market is now both mature and liquid, offering yields of 9% to 14% p.a. on works valued over $100,000.

* With central banks effectively working in a negative or near-zero interest rate environment, the Art Market looks very healthy by comparison, having posted a 1,955% growth in the annual auction turnover of its Contemporary segment over the past 19 years.

* These returns are not just reserved for 'star' artists. Our research finds a substantial average annual yield of approximately 7% on works sold above the €20,000 threshold.

* Considering these macro- and micro-economic data, the past 19 years have confirmed the Art Market's potential as a safe haven against economic and financial turbulence, generating substantial and recurring yields.

* The Internet with its galloping geographical ubiquity and its access by more than 5 billion people around the world (Microsoft data) is now the single most important marketplace for auction operators all over the world and is at the very core of their commercial strategies on all of the world's major continents. Almost 99% of the 6,300 auction firms in the world today have an Internet presence (compared with just 3% in 2005).

* Art represents a potent form of Soft Power that is vital for the United States, China and, at a different level, countries like Qatar and the United Arab Emirates.

* In short, the Art Market has all the characteristics of a historic, efficient and global market.

* The Internet with its galloping geographical ubiquity and its access by more than 5 billion people around the world (Microsoft data) is now the single most important marketplace for auction operators all over the world and is at the very core of their commercial strategies on all of the world's major continents. Almost 99% of the 6,300 auction firms in the world today have an Internet presence (compared with just 3% in 2005).

* Art represents a potent form of Soft Power that is vital for the United States, China and, at a different level, countries like Qatar and the United Arab Emirates.

* In short, the Art Market has all the characteristics of a historic, efficient and global market.

- TOP 20 artists - H1 2019 © Artprice by artmarket.com

* Artist “” Turnover (USD)

1 - Claude MONET (1840-1926) $251,165,100

2 - Pablo PICASSO (1881-1973) $243,085,600

3 - ZAO Wou-Ki (1921-2013) $155,827,800

4 - Andy WARHOL (1928-1987) $148,977,700

5 - ZHANG Daqian (1899-1983) $110,686,700

6 - Jeff KOONS (1955-) $103,501,700

7 - Paul CÉZANNE (1839-1906) $98,418,200

8 - WU Guanzhong (1919-2010) $95,895,200

9 - Francis BACON (1909-1992) $93,626,300

10 - Robert RAUSCHENBERG (1925-2008) $90,964,400

* Artist “” Turnover (USD)

1 - Claude MONET (1840-1926) $251,165,100

2 - Pablo PICASSO (1881-1973) $243,085,600

3 - ZAO Wou-Ki (1921-2013) $155,827,800

4 - Andy WARHOL (1928-1987) $148,977,700

5 - ZHANG Daqian (1899-1983) $110,686,700

6 - Jeff KOONS (1955-) $103,501,700

7 - Paul CÉZANNE (1839-1906) $98,418,200

8 - WU Guanzhong (1919-2010) $95,895,200

9 - Francis BACON (1909-1992) $93,626,300

10 - Robert RAUSCHENBERG (1925-2008) $90,964,400

11 - David HOCKNEY (1937-) $88,956,700

12 - Roy LICHTENSTEIN (1923-1997) $85,324,300

13 - Amedeo MODIGLIANI (1884-1920) $85,051,900

14 - Mark ROTHKO (1903-1970) $79,994,500

15 - René MAGRITTE (1898-1967) $76,110,700

16 - KAWS (1974-) $70,047,900

17 - Jean-Michel BASQUIAT (1960-1988) $65,796,000

18 - Gerhard RICHTER (1932-) $63,301,200

19 - Yayoi KUSAMA (1929-) $60,714,600

20 - Marc CHAGALL (1887-1985) $56,071,000

Source : Artprice by Art Market

Ruby BIRD

http://www.portfolio.uspa24.com/

Yasmina BEDDOU

http://www.yasmina-beddou.uspa24.com/

12 - Roy LICHTENSTEIN (1923-1997) $85,324,300

13 - Amedeo MODIGLIANI (1884-1920) $85,051,900

14 - Mark ROTHKO (1903-1970) $79,994,500

15 - René MAGRITTE (1898-1967) $76,110,700

16 - KAWS (1974-) $70,047,900

17 - Jean-Michel BASQUIAT (1960-1988) $65,796,000

18 - Gerhard RICHTER (1932-) $63,301,200

19 - Yayoi KUSAMA (1929-) $60,714,600

20 - Marc CHAGALL (1887-1985) $56,071,000

Source : Artprice by Art Market

Ruby BIRD

http://www.portfolio.uspa24.com/

Yasmina BEDDOU

http://www.yasmina-beddou.uspa24.com/

Ruby Bird Yasmina Beddou H1 2019 Art Market Report Artprice By Art Market Demand Contemporary Art Supply Contracts Prices Rise Public Sales Of Fine Art Paintings Sculptures Drawings Photographs Prints Installations

Liability for this article lies with the author, who also holds the copyright. Editorial content from USPA may be quoted on other websites as long as the quote comprises no more than 5% of the entire text, is marked as such and the source is named (via hyperlink).